- Point of view

Artificial intelligence in consumer banking

Most banks are excited about artificial intelligence (AI). They know it can provide significant benefits for the industry. But many still struggle to see the how it can be applied to their businesses. To address this question, we look at the business objectives consumer banks face today and how artificial intelligence can help to achieve them.

What business objectives do consumer banks face today?

Like many industries, consumer banks face five primary objectives:

- Grow revenue

- Manage risk and compliance

- Enhance customer experience

- Innovate to compete

- Reduce operating costs

Artificial intelligence can step in to help banks attain each one of these objectives.

How can artificial intelligence help?

Grow revenue

For decades, banks have used customer data, such as income, credit scores, and spending patterns to promote, cross-sell, and up-sell their products to grow revenue. But today's technologies allow banks to access more data and grow revenue in new ways.

Consider the banking journey of a millennial customer whose onboarding point to a bank was a college loan six years ago. Since then, his comfort with all things digital has increased, and his banking needs have evolved. The bank has kept tabs on his credit behavior through traditional databases and his monthly credit score. But something has fallen through the cracks – the trail of terabytes of behavioral and preferential data that he leaves via his digital journeys and payment behavior across products and services outside his student loan or relationship with the bank.

This customer may have recently purchased an engagement ring from a jeweler in the bank's network, a clear signal that he's planning to get married. As a result, he may be thinking of buying a home soon. Without listening to these digital signals, his need for a mortgage goes undetected unless he applies for one, putting the bank in a passive, reactive mode. Using AI and machine learning for faster, more granular analysis, the bank can proactively address the customer's latent needs by drawing compelling insights from his digital footprint and payment behavior.

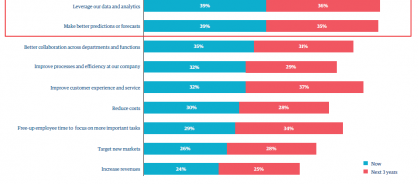

With AI, a bank can transform its predictive models. In fact, a recent study by Genpact confirms that senior banking executives believe that AI is generating, and will continue to generate, the greatest business benefits by leveraging data and analytics and making better predictions.

Figure 1: Current impact of AI seen on the ability to use data and improve forecasts

When decisioning is required at today's speed and scale, algorithms have to learn on the fly, which means data has to be instantaneously usable. It is for this reason that the industry's innovation outlook for the next five years is entirely AI-driven, from intelligent data platforms that put structure into data, to dynamic algorithms that continually learn about consumer preferences and intent as they crawl through data lakes and blockchains.

Enhance customer experience

For banks, enhancing the customer experience is critical. Alexa and Google Home are now common household companions, allowing consumers to enjoy great interactions. And people have come to expect the same level of service from their banks. AI-driven technologies can deliver highly personalized user experiences. Intelligent voice and chat bots, not available in a pre-AI era, are changing and reshaping how banks interact and communicate with clients. Like an Alexa for banking, personal digital assistants help consumers access a wealth of information on budgeting, saving for retirement, and more, tailored to their banking needs.

That said, a recent study by Genpact suggests that, while most senior executives believe customers will prefer to be served by a bot than a call center agent by 2021, the consumer perspective is much different. The disconnect may be because executives are responding to the cost-saving properties of bots, while consumers are responding to their perceptions or experiences with them.

Therefore, it is important for banks to keep in mind that smart assistants work best when integrated with other systems, allowing an end-to-end view of the customer. In a silo, the usefulness of these bots may be quickly exhausted, the insights they generate may be misleading, and the consumer may not perceive them as all that helpful or smart. Successful releases of virtual assistants are those with a rich knowledge and content base. Moving forward, we see these digital assistants providing not only basic transactional information, but also greater insight into, and advice to help promote, consumers' financial well-being – another reason why integration is important.

Manage risk and compliance

In an environment in which tighter compliance regulations challenge financial institutions, the ability to adapt can mean a distinct competitive advantage.

The variety of payment and investment systems available to consumers today (such as crypto-currencies, shared economy, and marketplace lending) have brought about a new era in money laundering. The cases are more complex, not just because there are now more hidden digital networks but also because there are so many creative ways laundering can be orchestrated interweaving traditional and digital means. Also, consumers are more easily used as unwitting accomplices. Traditional investigative work by operations analysts may no longer scale. In order to scale, the ability of analysts to gather and integrate data, and incorporate new data into their models quickly and efficiently, is key. Even then, there is no guarantee that previous analytics would still work, given everything that's new. Using a variety of methodologies, AI, by means of deep learning and computer vision, can explore the data and find patterns quickly, an impossible feat using traditional approaches.

Innovate to compete

AI helps banks compete. For example, AI presents an opportunity for consumer banks to democratize financial advice. Today, financial advice is mostly available in the form of expensive financial advisors for high-net-worth individuals who, ironically, may be less in need of such advice than people on more modest incomes. Meanwhile, everyday consumers leave financial breadcrumbs everywhere – when they swipe a card or pay a friend. Yet no one is picking up the crumbs and offering them advice. To differentiate themselves from their competitors, consumer banks can provide financial advice to everyday consumers. And with AI, banks can dramatically reduce the cost of offering such advice. In this respect, AI can help banks move from providing financial services to their customers to facilitating their financial betterment.

Reduce operating costs

Everyone wants to do more with less. Consumer banks are no exception. Banks can reduce costs by adopting new operating models that are more efficient while also enabling tighter controls. This is where artificial intelligence can step in to take on manual work that is routine and repetitive.

Teller transactions cost about 12 times more than mobile check deposits, and ATM transactions cost about three times more. Eliminating the need for a bank teller or ATM to process check deposits drives significant savings for the bank. When consumers deposit checks through their mobile phones, AI is at play in computer vision that's used to take the image of a check and process it. While check-image processing has been around for a while, advances in computer vision have made this process better than ever, for example, by accurately interpreting handwriting.

Similarly, AI powers intelligent chat bots that can respond to straightforward customer inquiries, such as resetting passwords and checking account balances. This reduces call-center volumes and operating costs.

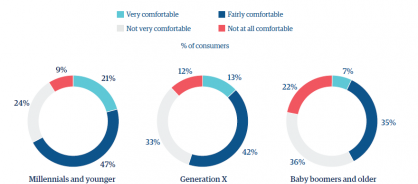

While it may seem that banks are removing the personal touch, they're actually increasing the level of personalization and improving consumers' journeys, thanks to insights captured from their digital footprints. In fact, using personal data for such customization is increasingly expected by consumers. As shown by the second edition of Genpact's recent research on AI, 68% of millennials and over 42% of older generations are comfortable with companies allowing AI to use their personal data to improve their customer experience.

Figure 2: AI and your personal data

How can banks move forward?

Double down on data

Banks already have at their disposal much of the information they need to start adopting AI today. What they may not have is all the data, or the right data, in the right place. A bank's various divisions and departments often have their own sets of client data in their own formats. So data management and data engineering are crucial. Having one, holistic view of the customer enables banks to connect the dots and predict customer needs that might not otherwise be readily apparent.

Be all-in on re-skilling

It takes some base data science knowledge to know the right data to use, how to tap it correctly, and how to fold it into current processes. Using data science to solve real problems and provide clear guidance on how to evaluate the costs and benefits of an AI application in consumer banking scenarios is critical. Coupling this data science with business knowledge is key. Ultimately, consumer banks that train their employees to be bilingual – confident moving between the fields of business and technology – are the ones that will prevail.

AI as the neural wiring

A recent study by Genpact shows that 99% of banking senior executives say their businesses have plans to implement AI by 2021. We are reaching the point where AI is no longer just on the fringes of an organization but at its core – the neural wiring. AI's potential to help banks grow revenue, manage risk, enhance customer experience, drive innovation, and lower cost is too large to ignore. The time to think in terms of AI-first business models in consumer banking is now.

Download the full report from the second edition of Genpact's research: AI 360: Insights from the next frontier of business.

Visit our consumer banking solutions page

Share