- Blog

Monitoring business spend in a world of new risks

The past couple of years has accelerated the need for enhanced spend monitoring procedures

Anu Priy Vij

Compliance as a Service Leader

Published

12/21/2021

Published

12/21/2021

Anu Priy Vij

Compliance as a Service Leader

Increased pressure to profit, shift in supply chains, changes in ways of working – these are just some of the new spend risks that have emerged due to COVID-19. But there's good news, too. Increasing adoption of digital technologies and advanced techniques can help companies manage risks in disbursements to employees and vendors more effectively than ever before.

That was the consensus of panelists who joined the Genpact webinar on monitoring business spend that was organized in partnership with Compliance Week. Sharing their expertise were Jenitha John, global board director of the Institute of Internal Auditors (IIA), Amber Starkey, global expense manager for Cardinal Health, and Daniel Lyjak, director of disbursements with the Zurich American Insurance company. I had the honor of joining this esteemed panel. Subhashis Nath, Genpact's service line leader for enterprise risk and compliance, moderated the discussion.

Emerging risks in the new normal

Several factors have contributed to increased risk exposure from business spend, most stemming from – but not limited to – the COVID-19 pandemic. The new risks include:

- Increased pressure to profit: Companies under pressure to boost revenue and profits can sometimes feel tempted to cut corners and resort to irregular practices

- Shift in supply chain: Nearly 94% of Fortune 1000 companies witnessed supply chain disruption due to COVID-19. In their rush to find new suppliers, companies might feel inclined to skimp on due diligence

- Increased government interaction: Corrupt officials can exploit the urgency companies face to acquire business-critical licenses and expedited clearances from customs and other government bodies

- Limited workforce: Layoffs have undermined compliance efforts due to reductions in the size of monitoring teams

- Increase in cash expenses: Amber surfaced a global trend when she said, "We saw some increased cash disbursements [to people working from home] because not everyone has a corporate card"

But while COVID-19 is responsible for some of these circumstances, "Market shocks can come from anywhere," Jenitha pointed out, "so having a strong expense management culture can help [companies] not just survive, but thrive."

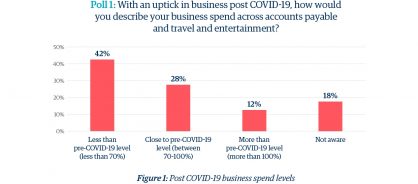

Breaking news: Spending is nearly up to pre-COVID-19 levels

We conducted a poll of webinar attendees to assess their current level of travel and entertainment (T&E) expenses. Nearly a third said travel and entertainment (T&E) spend was approaching pre-pandemic levels

The data supports the results – the US Transportation Security Administration (TSA) reports suggest that travel in Q3 2021 is already at 60% of pre-COVID times from Q3 2019, and continues to grow rapidly. "Once one business starts to travel, we believe other companies will increase travel at a much faster rate, which will trigger a domino effect," Amber explained.

Need to improve spend monitoring practices

Traditional methods for spend monitoring – including review of transactions before payments – are not enough to manage new risks, the group agreed. Most prepayment tools and technologies analyze each expense in isolation. However, fraud and corruption do not present themselves on a single invoice/expense; they can prove complex and become identified over time, across multiple cases and multiple employees. Any reviews performed on individual transactions will likely fail to uncover any significant risk or influence employee behaviors to prevent future leakages.

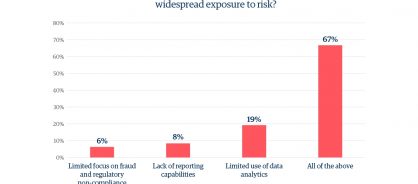

Our attendees agreed. When asked what limitations they were experiencing in their existing spend monitoring practices that were exposing them to risk, nearly 20% pointed to limited use of data analytics

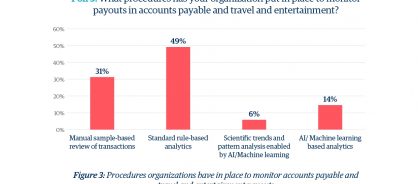

Our final poll question asked attendees about current procedures their companies use to monitor payouts in accounts payable (AP) and T&E. Only 14% said they employed AI and machine-learning-based analytics, while a mere 6% applied scientific trends and pattern analysis enabled by AI and machine learning (see figure 3 below). The vast majority – 80% – continue to rely on manual samples or standard rule-based reviews to monitor transactions.

A case for data analytics

The numbers call for improvement, our panelists agreed. The right approach, they concurred, is to set up a continuous transaction monitoring program fortified with analytics that identify non-compliance across a wide range of high-risk categories. The application of behavioral science can further help identify patterns of non-compliance and catch repeat offenders. Finally, there should be a single source of truth to view all information through easy-to-access dashboards.

Such well-conceived data analytics can go far to resolve a wide array of issues, said Jenitha, who advises auditors to perform a fraud risk assessment that addresses vulnerabilities before breaches occur. Additionally, not only does more sophisticated analytics help management make better decisions, IIA standards recommend their use. Analytics track trends and patterns – such as weekend spend and duplicate or repetitive payments – that teams might otherwise miss.

Our panelists discussed cases in which successful pattern analysis flagged unusual entertainment spend with an external attendee, identified a gap in the employee separation process by tracking sudden spikes in spending, and exposed employees who were claiming fraudulent expenses suspiciously just short of the threshold defined by policy.

The benefits of comprehensive spend monitoring

The webinar concluded with the panel summing up the benefits of a comprehensive, digitized spend monitoring program. They cited the following advantages:

- Reduced audit cost due to fewer manual procedures while maintaining or even enhancing risk coverage

- Wider coverage across policy, fraud, and regulatory risks thanks to a 100% analytics-based transaction review process

- Fewer prosecutions and penalties because companies can routinely meet all guidelines

- Best-in-class practices through cross-company process and policy standardization

- Deeper insights from high-risk red flag testing

Amber noted: "In three months, we had already met our (target) ROI on third-party due diligence from all the post-payment findings in both AP and T&E."

The message is loud and clear. COVID-19 may have forced companies to face new and diverse risks in business spend, but the future-forward policy and digital updates firms make today will stand them in good stead long after the pandemic recedes.

Share